There are some industry pundits

claiming that residential home values have risen too quickly and that current

levels are on the verge of another housing bubble. It is easy to see how this

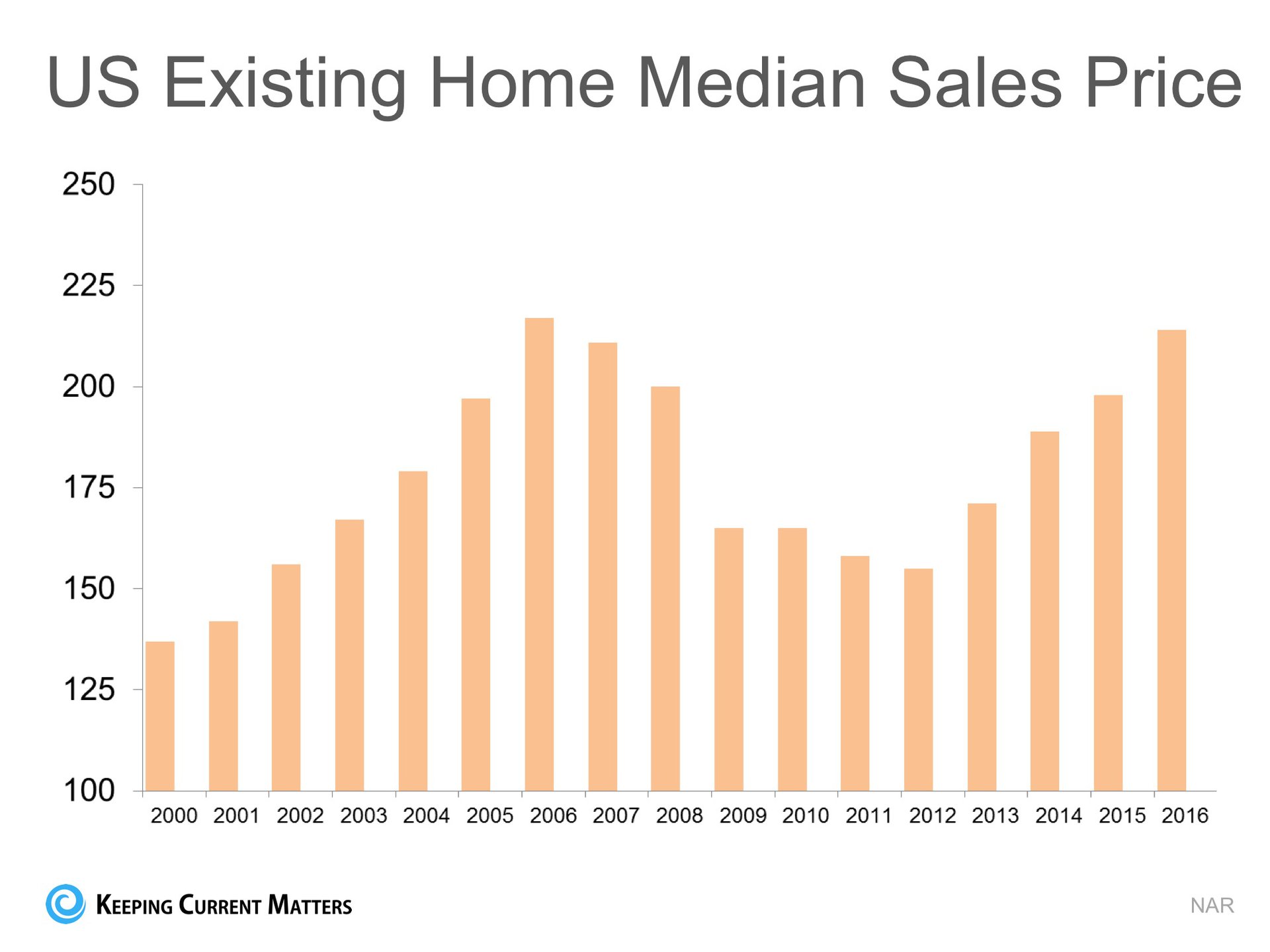

thinking has taken form if we look at a graph of home prices from 2000 to

today.

The graph definitely looks

like a rollercoaster ride. And, as prices begin to reach 2006 levels again,

it "seems logical" that the next part of the ride would be

downhill. However, this graph includes the anomaly of the price bubble and

the correction (the housing crash).

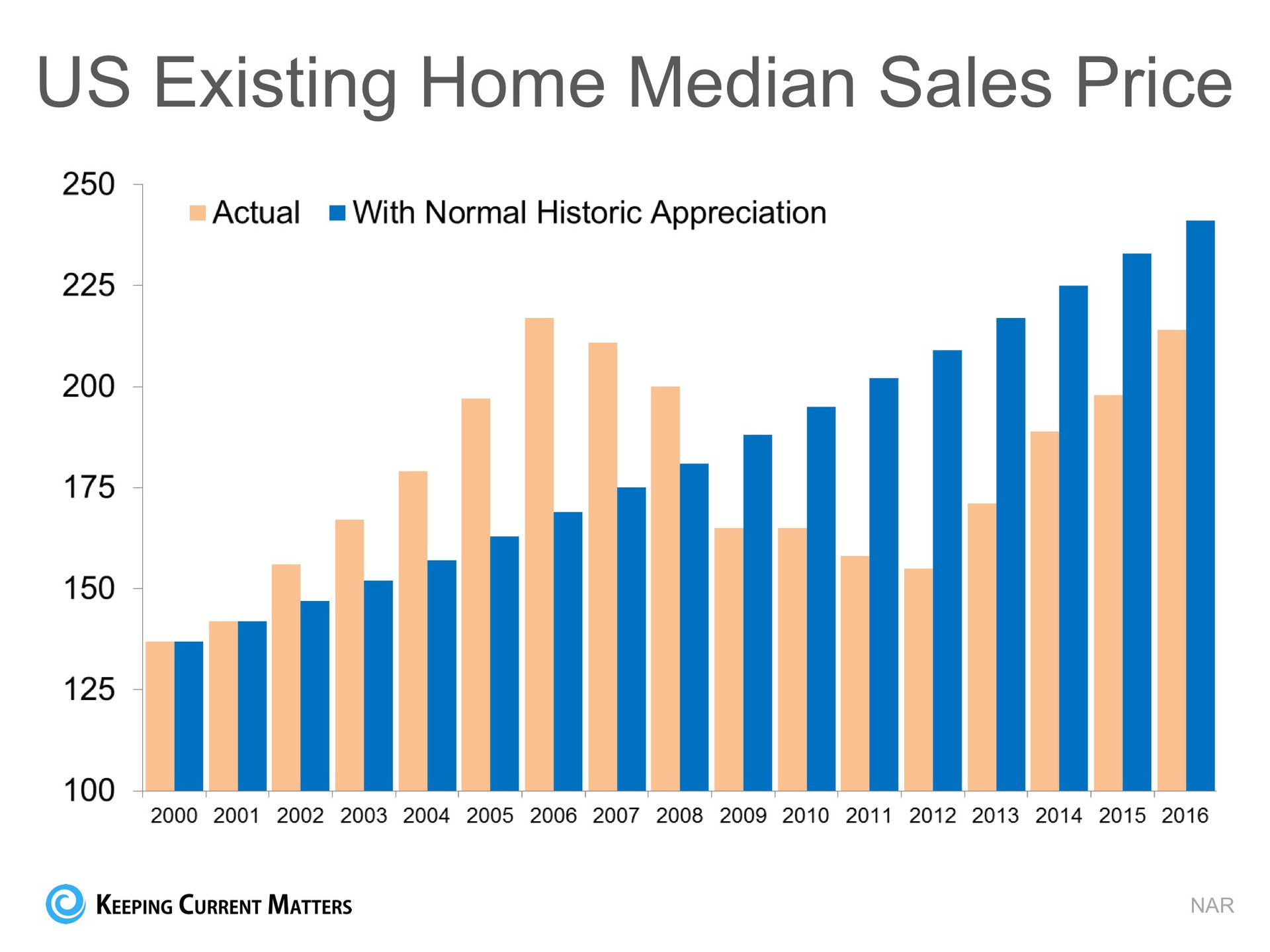

What if the bubble & bust didn't occur?

Let's

assume that instead of the rise and fall in home prices that we saw last

decade, we just had normal historic appreciation from 2000 to today.

According to the 100+ experts that are surveyed for the Home Price

Expectation Survey, normal annual appreciation for residential single

family homes from 1987 to 1999 was 3.6%. Starting with the median home price

in 2000, we added 3.6% to it each year since then. Here is that graph

intermixed with the above graph.

What this shows us is

that, had the bubble and crash not occurred and instead we just had normal

annual appreciation over this period, prices would actually be greater than

they are today.

Bottom Line

There

is no reason for alarm as prices seem to be right in line with where they

should be.

|

Wednesday, August 31, 2016

Home Values: DEFINITELY NOT in Bubble Range!!

Tuesday, August 30, 2016

WHY IS THERE SO MUCH PAPERWORK TO SIGN TO GET A MORTGAGE?

We are often asked why there is so much paperwork mandated by the bank for a mortgage loan application when buying a home today. It seems that the bank needs to know everything about us and requires three separate sources to validate each and every entry on the application form. Many buyers are being told by friends and family that the process was a hundred times easier when they bought their home ten to twenty years ago. There are two very good reasons that the loan process is much more onerous on today's buyer than perhaps any time in history. 1. The government has set new guidelines that now demand that the bank prove beyond any doubt that you are indeed capable of affording the mortgage.

During

the run-up in the housing market, many people 'qualified' for mortgages that

they could never pay back. This led to millions of families losing their

home. The government wants to make sure this can't happen again.

2. The banks don't want to be in the real estate business.

Over

the last seven years, banks were forced to take on the responsibility of

liquidating millions of foreclosures and also negotiating another million

plus short sales. Just like the government, they don't want more

foreclosures. For that reason, they need to double (maybe even triple) check

everything on the application.

However, there is some good news in the situation.

The

housing crash that mandated that banks be extremely strict on paperwork

requirements also allows you to get a mortgage interest rate as low as 3.43%,

the latest reported rate from Freddie

Mac. The friends and family who bought homes ten or twenty ago

experienced a simpler mortgage application process but also paid a higher

interest rate (the average 30 year fixed rate mortgage was 8.12% in the

1990's and 6.29% in the 2000's). If you went to the bank and offered to pay

7% instead of less than 4%, they would probably bend over backwards to make

the process much easier.

Bottom Line

Instead

of concentrating on the additional paperwork required, let's be thankful that

we are able to buy a home at historically low rates.

|

Monday, August 29, 2016

Don't Get Caught in the Rental Trap!

There are many benefits to home ownership. One of the top ones is being able to protect yourself from

rising rents and lock in your housing cost for the life of your mortgage.

Don't Become Trapped

Jonathan

Smoke, Chief Economist at realtor.com, reported

on what he calls a "Rental Affordability Crisis." He warns

that,

"Low

rental vacancies and a lack of new rental construction are pushing up rents,

and we expect that they'll outpace home price appreciation in the year

ahead."

In

the Joint Center for Housing Studies at Harvard University's 2015 Report

on Rental Housing, they reported that 49% of rental households are

cost-burdened, meaning they spend more than 30% of their income on housing.

These households struggle to save for a rainy day and pay other bills, such

as food and healthcare.

It's Cheaper to Buy Than Rent

In

Smoke's article, he went on to say,

"Housing

is central to the health and well-being of our country and our local

communities. In addition, this (rental affordability) crisis threatens the

future value of owned housing, as the burdensome level of rents will trap

more aspiring owners into a vicious financial cycle in which they cannot save

and build a solid credit record to eventually buy a home." "While more than

85% of markets have burdensome rents today, it's perplexing that in more than

75% of the counties across the country, it is actually cheaper to buy than

rent a home. So why aren't those unhappy renters choosing to buy?"

Know Your Options

Perhaps

you have already saved enough to buy your first home. HousingWire reported

that analysts at Nomura believe:

"It's

not that Millennials and other potential homebuyers aren't qualified in terms

of their credit scores or in how much they have saved for their down payment. It's that they

think they're not qualified or they think

that they don't have a big enough down payment." (emphasis added)

Many

first-time homebuyers who believe that they need a large down payment may be holding

themselves back from their dream home. As we have reported before,

in many areas of the country, a first-time home buyer can save for a 3% down

payment in less than two years. You may have already saved enough!

Bottom Line

Don't

get caught in the trap so many renters are currently in. If you are ready and

willing to buy a home, find out if you are able. Have a professional help you

determine if you are eligible to get a mortgage.

|

Subscribe to:

Posts (Atom)